The System Map

If you only understood one thing about venture, it's this

The more clearly we see the operating system and the narrative around it, the more intelligently we can work with it or build alongside it. So let’s deep dive into the intricacies of venture!

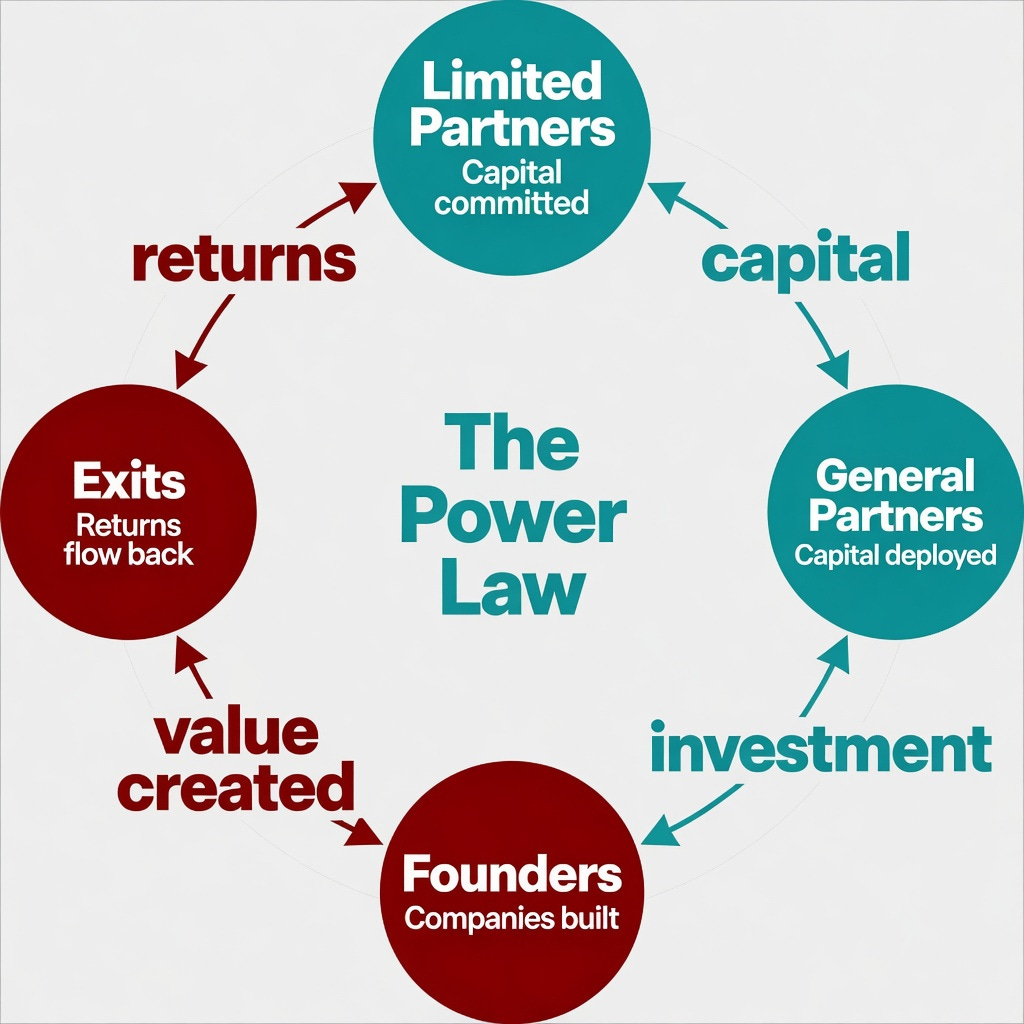

The visible chain

The structure of venture capital is not especially complicated on the surface. Limited Partners (LPs) — the pension funds, university endowments, family offices, sovereign wealth vehicles — commit capital to a fund. General Partners (GPs) manage that fund, deploy it into early-stage companies, and try to return it many times over. Founders receive the capital, build the companies, and (if everything goes to plan, and sometimes even of it doesn’t) generate the exits that flow back up the chain.

Straightforward and even elegant.

However, what the diagram doesn't show is the logic that drives behaviour through every link in the chain.

The power law

Most people who encounter the power law (this concept was introduced in the previous article) for the first time do so as a statistical observation. They learn that in venture, outcomes are not distributed normally. They are distributed wildly: a tiny number of investments generate the overwhelming majority of returns.

Only once you dig down a bit deeper, the numbers are quite startling. As Marc Andreessen, speaking at Stanford’s Graduate School of Business in March 2014, noted “of the roughly 200 companies funded by top-tier VCs each year, as few as fifteen will generate approximately 95% of the returns for the entire category in that vintage year.”

The invisible link.

The power law is not an investment strategy per se. It is a belief about the nature of technological change.

The people who built venture capital as a discipline started from the premise that truly transformative companies — the ones that do not merely improve on what exists but replace it with something the world did not know it needed — are, by their nature, rare. They cannot be manufactured on a schedule. And when they do appear, they tend to generate returns that are not merely large but categorically different in magnitude from everything else in the portfolio.

The model is built backwards from this observation. If one company can return the entire fund then the correct response is not to protect against failure. It is to ensure you are in the room when that company walks through the door.

This is why a GP will pass on a perfectly good business that will reliably return two or three times the investment. Not out of arrogance or greed. But because a fund built on predictable, moderate outcomes cannot survive the mathematics of the asset class. The hurdle rate (the minimum return a venture fund must achieve to meet investor expectations and justify risk), the carry structure, the LP expectations — all of it demands that somewhere in the portfolio, there is a company growing at a rate that looks insane.

Peter Thiel put it plainly: “The biggest secret in venture capital is that the best investment in a successful fund equals or outperforms the entire rest of the fund combined.” He invested $500,000 in Facebook. It returned approximately $1.1 billion.

What does it mean in the chain

Once you see this clearly, the behaviour at every level of the chain makes a lot more sense.

LPs accept illiquidity and probable near-term losses because they are not optimising for the performance of any individual company, or even any individual fund. They are optimising for the tail. The rare, extraordinary outcome that offsets everything else. University endowments and sovereign wealth funds can absorb a decade of lock-up because they are playing a longer game than almost any other investor class. Venture is the part of the portfolio built to be patient enough for something implausible to happen.

GPs chase what looks like irrational valuations, fund companies that are burning money at speed, and hold their nerve through years of apparent underperformance because they are managing around a single statistical reality: missing the one winner hurts more than losing on everything else. The asymmetry is not just mathematical. It is reputational. A fund that backed Uber, even if half its other bets failed, raises its next fund. A fund of steady, sensible returns that never touched anything extraordinary — does not.

Founders who receive venture backing are not simply getting capital. They are entering an implicit agreement that the expected outcome is something closer to extraordinary. The GP needs this from them. The LP needs this from the GP. The whole chain is built around the principle that only exponential ambition is, within this particular system, structurally useful.

Yes, and…

The strongest criticism of venture power-law thinking is that it risks becoming deterministic: transforming a statistical regularity into a worldview that explains every decision after the fact and leaves little room for alternative models of value creation. Viewed from the outside, venture can sometimes resemble a discipline that has taken a map and slowly turned it into a rulebook.

This becomes especially intriguing because power laws describe outcomes, but outcomes and strategies are not quite the same thing. The existence of a few spectacular winners does not necessarily imply that every investment decision ought to be organised around the pursuit of extreme outliers. Yet in venture, the distinction occasionally appears to blur.

There is also the small matter of survivorship bias — venture’s best magic trick. History has a tendency to spotlight Facebook and Google while politely ushering thousands of similarly ambitious failures out through the side door. Looking backwards, success is suspiciously neat. Stories become coherent, decisions appear inevitable, and patterns line up with the tidy elegance of a Poirot ending, where chaos suddenly rearranges itself into inevitability. One begins to wonder whether some of venture’s deepest insights are genuinely predictive, or merely very persuasive after the fact.

Then there is the structure itself. The pursuit of oversized outcomes may owe as much to the machinery of venture—management fees, carry structures, LP expectations, and fixed fund cycles—as to any natural law governing innovation.

And perhaps most curious of all is the industry’s relationship with unpredictability. Venture mythology often treats transformative companies as bolts of lightning — rare, dazzling events appearing without warning. Yet modern startup culture appears to spend an extraordinary amount of energy attempting to manufacture precisely this unpredictability. Entire ecosystems now exist to produce founders through playbooks, accelerators, frameworks, and repeatable templates for success. If breakthroughs are truly unknowable, it seems an awfully organised effort devoted to making them happen at scale.

The remarkable bit

Venture capital is, at its core, an institutionalised mechanism for funding things that have no evidence yet. It is the only asset class structurally built to be wrong most of the time, and to remain viable anyway. It works because the rare wins are large enough to justify the consistent losses but also because the rare wins are, in the most literal sense, new things in the world.

The internet. Social networks. Smartphones. Genomic medicine. Clean energy infrastructure. None of these were obvious at the time of the initial bet. All of them had the shape of things that would almost certainly fail. The investors who backed them were not clairvoyant. They were operating within a system designed to tolerate being wrong, repeatedly so, in exchange for the occasional chance to be transformatively right.

The one thing

So, if you only understood one thing about venture capital, I would want it to be this:

The key to decode otherwise confusing VC behaviours such as aggressive pricing, FOMO, chasing large markets, is the understanding of a genuine belief about how transformative change happens.

Progress, it turns out, does not arrive on a normal distribution. It concentrates. It arrives in improbable bursts, through improbable people, at moments that looked, in advance, entirely unpromising.

Venture capital is the financial architecture built around that observation. And whatever its flaws it has managed to channel capital towards companies that no other mechanism would have touched.

As always, I’d love to know which part of this landed differently than you expected. The comments are open.

Next time: what happens when the power law meets AI — and whether the model that made venture work is about to be rewritten entirely.

References

Andreessen, M. (2014) ‘Marc Andreessen’s view from the top’, The Stanford Daily, 5 March. Available at: https://stanforddaily.com/2014/03/05/marc-andreessens-view-from-the-top-part-1-of-2

See also: Stanford Graduate School of Business (no date) Marc Andreessen: ‘We are biased toward people who never give up’. Available at: https://www.gsb.stanford.edu/insights/marc-andreessen-we-are-biased-toward-people-who-never-give

Evans, B. (2016) ‘In praise of failure’, ben-evans.com, 28 April. Available at: https://www.ben-evans.com/benedictevans/2016/4/28/winning-and-losing

Iskold, A. (2021) 4 essential truths about venture investing. TechCrunch, 24 February. Available at: https://techcrunch.com/2021/02/24/4-essential-truths-about-venture-investing

Klingler-Vidra, R. (2022) ‘Book Review: The Power Law: Venture Capital and the Art of Disruption by Sebastian Mallaby’, LSE Review of Books. Available at: https://blogs.lse.ac.uk/lsereviewofbooks/2022/02/23/book-review-the-power-law-venture-capital-and-the-art-of-disruption-by-sebastian-mallaby/

Metiquity (2025) Demystifying venture capital investing. Available at: https://metiquity.ca/post/Demystifying-Venture-Capital-Investing [Secondary source reporting Correlation Ventures study of 21,640 financings, 2004–2013.]

Thiel, P. and Masters, B. (2014) Zero to one: notes on startups, or how to build the future. New York: Crown Business, p. 86.